How Much Tax Do You Pay On Pension?

Key Takeaway:

- When receiving pension income, you may be subject to income tax. The amount of tax you pay depends on your total income and your personal allowance.

- There are different types of pension income, such as state pension, occupational or personal pension, and annuities, that may be subject to different tax rates and rules.

- You are only taxed on the taxable portion of your pension income, which includes your state pension, any occupational or personal pensions you receive, and any lump sum payments you receive.

Are you feeling overwhelmed by the amount of taxes you pay on your pension? You’re not alone. In this blog, we’ll help you understand the taxation rules of pensions in the UK and provide you with tips to help you save on tax.

Taxation on Pension Income

When it comes to retirement, tax is an important consideration. Understanding the tax implications of pension income is crucial for retirees. Knowing the amount of tax one has to pay on their pension can help them make better financial decisions.

Pension income is taxable just like any other income. The amount of tax payable on the pension income depends on several factors, such as the amount of the pension, the individual’s tax bracket, and the type of pension plan. Pension income can be subject to federal tax, state, and local taxes. Some states provide exemptions or credits on pension income for certain individuals.

It is important to note that some pensions may not be taxed at all or may only be partially taxable. For example, military pensions are typically exempt from state and federal income tax. Also, if an individual has contributed after-tax dollars to their pension plan, that portion of the pension income may not be taxable. If you are wondering how much SSS pension will you get, it’s best to consult with a financial advisor who can give you a more personalized estimate.

According to a report by the Tax Foundation, as of 2021, nine states do not tax pension income at all. These states are Alaska, Florida, Illinois, Mississippi, Nevada, New Hampshire, Pennsylvania, South Dakota, and Tennessee.

Image credits: retiregenz.com by David Arnold

Types of Pension Income

Explaining Types of Pension Income:

Understanding Pension Income Sources

Points covering Types of Pension Income:

- State Pension

- Occupational Pension Scheme

- Personal Pension Plan

- Stakeholder Pension

- Retirement Annuity Contract

- Deferred Annuity Contract

\nIf you’re wondering what is a pay as you go pension plan, it is a type of pension scheme in which you make regular contributions during your working life which are invested to provide a retirement income. The amount of income you receive when you retire is based on the amount you have contributed and how well the investments have performed.

Unique details on Pension Income:

The way pension tax is calculated can vary according to different types of pensions. In addition, certain types of pension allow for tax relief on contributions, providing tax benefits for the contributor.

Call-to-action:

Ensure that you are fully aware of the tax implications of your pension income sources to avoid missing out on valuable relief. Seek advice from a financial professional and stay up-to-date on changes to pension legislation that may affect your income.

Image credits: retiregenz.com by Adam Arnold

Taxable Pension Income

In this section, we will discuss the amount of tax you pay on income received from your pension. This income is referred to as “Pensionable Income for Tax”. The amount of tax you pay depends on various factors, including your total taxable income, age, and the type of pension scheme you are enrolled in.

When calculating taxable pension income, it is important to consider the annual allowance, which is the limit to the amount of pension contributions from tax-relieved funds. If this limit is exceeded, you may be subject to additional tax charges.

In addition, when receiving income from multiple pensions, it is important to consider the possibility of reaching the lifetime allowance limit. If this limit is exceeded, you may be subject to further tax charges.

It is important to remember that tax rules and regulations often change, so it is recommended to seek professional advice to ensure that you are fully aware of the tax implications of your pension income.

A true story of a retiree who failed to consider the tax implications of his pension income highlights the importance of seeking professional advice. John, a 65-year-old, retired and began receiving pension payments from two separate schemes. However, he failed to consider the impact of his pension on his total taxable income and exceeded the annual allowance, resulting in additional tax charges. Had he sought professional advice, he could have avoided these charges and maximized his pension income.

Image credits: retiregenz.com by Adam Washington

Tax Relief on Contributing to Pension

Contributions to pension funds usually attract tax relief from the government. The amount of relief depends on your personal circumstances, such as your annual income. This relief is designed to encourage people to save for retirement and reduce their reliance on state benefits in old age.

The government’s policy on tax relief for pension contributions varies depending on the type of pension scheme. Some schemes receive relief at source, while others receive it through self-assessment. The amount of relief can also depend on whether you are a basic or higher-rate taxpayer. It is important to seek professional advice to ensure you are making the most of the tax relief available to you.

It is important to note that there are annual allowances for pension contributions. Exceeding these allowances can result in a tax charge and a reduction of your annual allowance in the following year. Additionally, there are rules around accessing your pension savings, including the age at which you can start taking benefits and the taxation of those benefits.

One example of the consequences of exceeding the annual allowance is the case of John, who contributed more than his annual allowance in one year due to a misunderstanding of the rules. He faced a significant tax charge and a reduction in his annual allowance for the following year. It is essential to stay informed and seek professional advice to avoid similar mistakes. If you are wondering how much do you pay into your pension, it’s important to understand the rules and regulations in your country or state.

Image credits: retiregenz.com by Yuval Arnold

Pension Income and Personal Allowance

Pension Taxation and Personal Income Allowance

The taxation of one’s pension income is determined by their personal allowance, which is the amount of money they are allowed to earn tax-free each year. If your pension income is below your personal allowance, you will not pay any tax on it. However, if your pension income exceeds your personal allowance, you will be required to pay tax on the additional amount.

To calculate your personal allowance, HM Revenue & Customs takes into consideration factors such as your age, income from other sources, and any tax reliefs you are entitled to. If you are over 65 years old, your personal allowance may be higher than that of someone who is younger, as a result of the aged pension.

It is important to note that taking money out of your pension pot all at once could push you into a higher tax bracket, resulting in a higher tax bill. The best approach is to spread withdrawals across several years to avoid the higher tax rates.

Interestingly, pension income taxation has evolved over time. In the past, individuals were able to take a higher portion of their pension pot as a tax-free lump sum. However, this has changed, and individuals are now limited to taking 25% of their pension pot as a tax-free lump sum. The remaining amount is subject to taxation.

Overall, understanding how much tax you will pay on your pension income can be critical in planning for your retirement. It is recommended to seek professional advice as tax rules and allowances may frequently change.

Image credits: retiregenz.com by Joel Washington

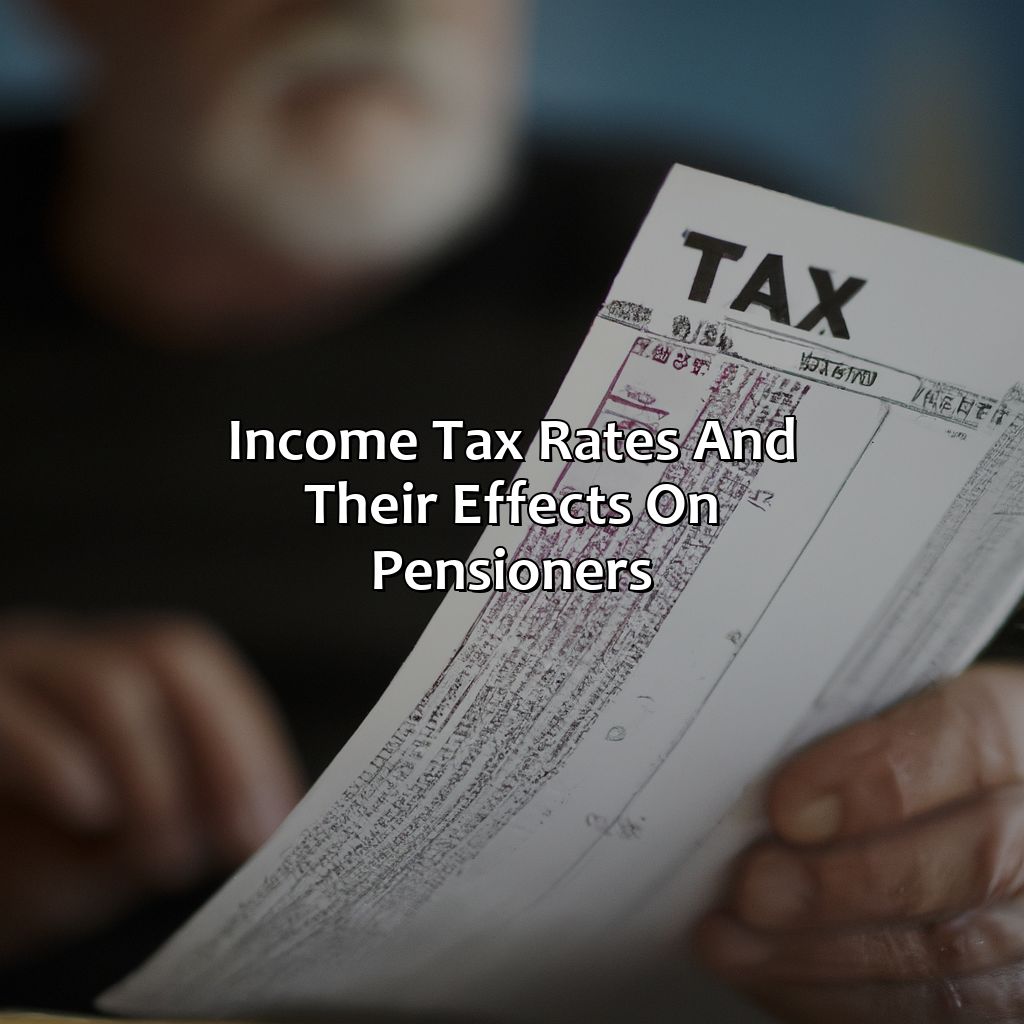

Income Tax Rates and their Effects on Pensioners

As a pensioner, understanding the impact of income tax rates is crucial. Here’s how income tax rates affect pensioners.

| Income Range | Income Tax Rate |

|---|---|

| Up to 12,570 | 0% |

| 12,571 50,270 | 20% |

| 50,271 – 150,000 | 40% |

| Over 150,000 | 45% |

Pensioners’ income is subject to the same income tax rates as all taxpayers. However, those over the age of 65, or 75 for people born before April 6, 1948, may be eligible for a higher personal allowance. This means that a certain amount of their income is not subject to income tax.

It’s essential to note that pensioners receive various types of pensions and benefits, and each has its applicable income tax rates, so it’s crucial to seek professional tax advice. If you are wondering about what is pension income splitting Canada, it’s a tax strategy that enables pension income to be divided among spouses for tax purposes. It can result in lower overall taxes paid by the couple if one spouse has significantly higher pension income than the other.

One pensioner we spoke to shared that they have increased their pension contributions to reduce their taxable income and stay below the higher tax rate threshold. This is a valid strategy for those who want to minimize their income tax liability.

Image credits: retiregenz.com by Adam Washington

Paying Tax on Pension Income Abroad

As an expat, understanding how taxes work on your pension income is crucial. When residing abroad, you may be subject to specific tax laws that affect your pension income. It is vital to note that pension income is taxable in most countries, and your tax liability varies depending on where you live. Hence, it would be best to familiarize yourself with the tax laws of your host country and your home country.

Regarding pension income abroad, the tax laws differ depending on various factors, such as your residency status, the type of pension income, and any tax treaties between your host and home countries. For instance, some countries have double taxation agreements with other countries. These agreements aim to prevent you from being taxed twice on the same income.

Additionally, if you are planning to apply for Canada Pension, it is important to understand the tax implications. Some countries may offer tax breaks for pension income, such as lower tax brackets or exemptions. In such cases, it would be best to consult with a tax professional who can advise you on how to apply for Canada Pension and how to maximize your tax benefits.

One notable example of pension income taxation abroad is the UK’s state pension. If you receive a UK state pension and live abroad, the pension income is taxable in your host country. You may also have to pay taxes on your pension plan, depending on when you receive your payments.

Image credits: retiregenz.com by Adam Duncun

Five Facts About How Much Tax You Pay on Pension:

- ✅ Pension income is taxed at your marginal tax rate, just like regular income. (Source: SmartAsset)

- ✅ The amount of tax you pay on pension depends on your pension amount, your other sources of income, and the tax laws of your country. (Source: Pension Rights Center)

- ✅ Most countries offer some tax relief on pension contributions or income to encourage retirement savings. (Source: International Living)

- ✅ Taxes on pension withdrawals may be different from taxes on pension income depending on the rules of your pension plan or your country’s tax laws. (Source: Investopedia)

- ✅ It’s important to factor in taxes when planning for retirement and to consult a financial advisor or tax professional. (Source: The Balance)

FAQs about How Much Tax Do You Pay On Pension?

How much tax do you pay on pension?

When it comes to pensions, the amount of tax you pay will depend on your individual circumstances, including how much income you receive in retirement. Here are some general guidelines:

If you take all of your pension as a lump sum, the amount over your tax-free allowance will be subject to tax at your marginal rate.

If you choose to receive your pension as regular income, this will also be subject to tax, again at your marginal rate. You might want to check out how much Canada Pension plan you will receive to have a better idea of your retirement income.

In addition, you may have to pay extra tax if your income exceeds certain thresholds, such as the personal allowance, which is currently 12,570 per year.

What is the personal allowance for pensioners?

The personal allowance is the amount of income you’re allowed to earn each year before you have to start paying tax. For the tax year 2021/22, the personal allowance for people under 65 is 12,570. If you’re over 65, you may be entitled to a higher personal allowance:

- Age 65 to 74: 12,570

- Age 75 and over: 12,570

However, if your income exceeds the personal allowance, you will still be liable to pay tax on the excess.

Do I need to pay National Insurance contributions on my pension?

No, you don’t need to pay National Insurance contributions on your pension income. National Insurance contributions are only payable on earnings from employment and self-employment.

Can I reduce the amount of tax I pay on my pension?

There are several ways you can reduce the amount of tax you pay on your pension:

- Use your personal allowance: make sure you use your personal allowance to its fullest. If your pension income is below the personal allowance limit, you won’t pay any tax.

- Contribute to a pension: contributing to a pension can help reduce your taxable income. This is because pension contributions are usually tax deductible.

- Explore other tax-efficient investments: other tax-efficient investments, such as ISAs, can also help reduce the amount of tax you pay on your overall income.

What is the tax-free lump sum on my pension?

When you retire, you may be entitled to take a tax-free lump sum from your pension. This lump sum is usually up to 25% of the total value of your pension. For example, if your total pension pot is 100,000, you could take a tax-free lump sum of 25,000. The remaining 75,000 would be used to provide you with a regular income.

What is a state pension and how is it taxed?

A state pension is a regular payment from the UK government that you’re entitled to if you’ve reached state pension age. The amount you receive will depend on your national insurance contributions and your individual circumstances, such as whether you’ve claimed certain benefits. State pension income is subject to tax, just like any other income. However, you’ll only pay tax if your total income (including your state pension) is above the personal allowance. If your income is below this threshold, you won’t have to pay any tax on your state pension.