Checkout this IRS Loophole

Checkout this IRS Loophole

How To Draw Social Security Early?

Key Takeaway:

- To be eligible for early Social Security, you must meet age and income requirements. Individuals can claim benefits as early as 62 years old, but their monthly benefits will be reduced. To avoid reduction, you must not earn more than the income limits set by the Social Security Administration (SSA).

- The SSA calculates the reduction of benefits based on the number of months you receive payments before reaching your full retirement age. Generally, the earlier you claim, the greater the reduction. It’s important to consider the amount of reduction and how it will affect your long-term benefits before claiming early Social Security.

- You can apply for early Social Security benefits online or in-person. The online application process is convenient and takes about 15 minutes to complete. You can also apply in-person at your local Social Security office, but the process may take longer.

- Before claiming early Social Security, it’s important to consider your lifetime earnings, which can impact your benefits. You should also consider spousal and survivor benefits, which can provide additional income. It’s important to make an informed decision based on your personal financial situation and long-term goals.

Feeling the need to retire and tap into your social security savings? You’re not alone. Withdrawing social security early is an increasingly popular option for those who need financial security sooner. Learn how to navigate the process and get the most out of your social security benefits.

Eligibility Requirements for Early Social Security

To figure out if you can get early social security, you need to know the eligibility rules. Age Requirements and Income Limits are the two key factors. Learn all the details for these two sections. Then, find out if you’re eligible and plan your finances accordingly.

Image credits: retiregenz.com by David Woodhock

Age Requirements for Early Social Security

Drawing Social Security early is based on specific age requirements. You can opt for social security retirement benefits before reaching full retirement age, which is 67 years old for people born after 1960. The earliest one can get their first social security benefit is at the age of 62, but the monthly benefit will be lesser compared to if the individual waited until full retirement age.

If you opt to draw social security early, it reduces your benefit by a certain percentage of what you’d receive if you had waited to retire at Full Retirement Age (FRA). Your FRA depends on your birth date. You can calculate your exact FRA easily by using the Social Security Administration’s online calculator tool. Moreover, if the recipient continues to work and earns a high income while drawing benefits earlier than FRA, they may face further reductions in those monthly payments.

It’s also possible to draw from a deceased spouse’s or ex-spouse’s earning history as early as age 60 years old. Still, this path affects their future survivor benefits later on in life potentially.

According to SSA data, over 1 million people applied for early Social Security benefits in February 2020 alone.

Looks like retiring early comes with some strings attached – or should I say income limits?

Income Limits for Early Social Security

Social Security Income Limits for Early Retirement

For those considering early retirement, there are specific income limits to consider in order to be eligible for Social Security benefits. These limits differ depending on various factors including age, estimated retirement benefit and current income. It’s vital to understand the intricate details of these limits before applying for early Social Security.

In order to grasp a better understanding of the complex eligibility requirements, let’s have a closer look at the table below that outlines the income limits for Social Security early retirement based on different age groups:

| Age | Maximum Annual Income |

|---|---|

| 62 and younger | $18,960 |

| 63-65 | $50,520 |

As shown above, the maximum annual income limit for individuals aged 62 and under is set at $18,960. For individuals between ages 63-65 years old, this limit increases to $50,520. Exceeding these amounts can significantly impact your eligibility for early benefits.

It’s crucial to remember that although you may be eligible for early retirement with Social Security benefits if you meet certain criteria such as length of service or permanent disability status – it’s best to speak with an expert in this field before making any hasty decisions.

It was only recently when The Coronavirus Aid, Relief and Economic Security (CARES) Act was passed—a comprehensive stimulus bill designed to provide relief due to the global pandemic—making several changes regarding social security that have now come into law.

Calculating benefits for early social security is like playing a game of Jenga—remove a block too soon and the whole stack comes crashing down.

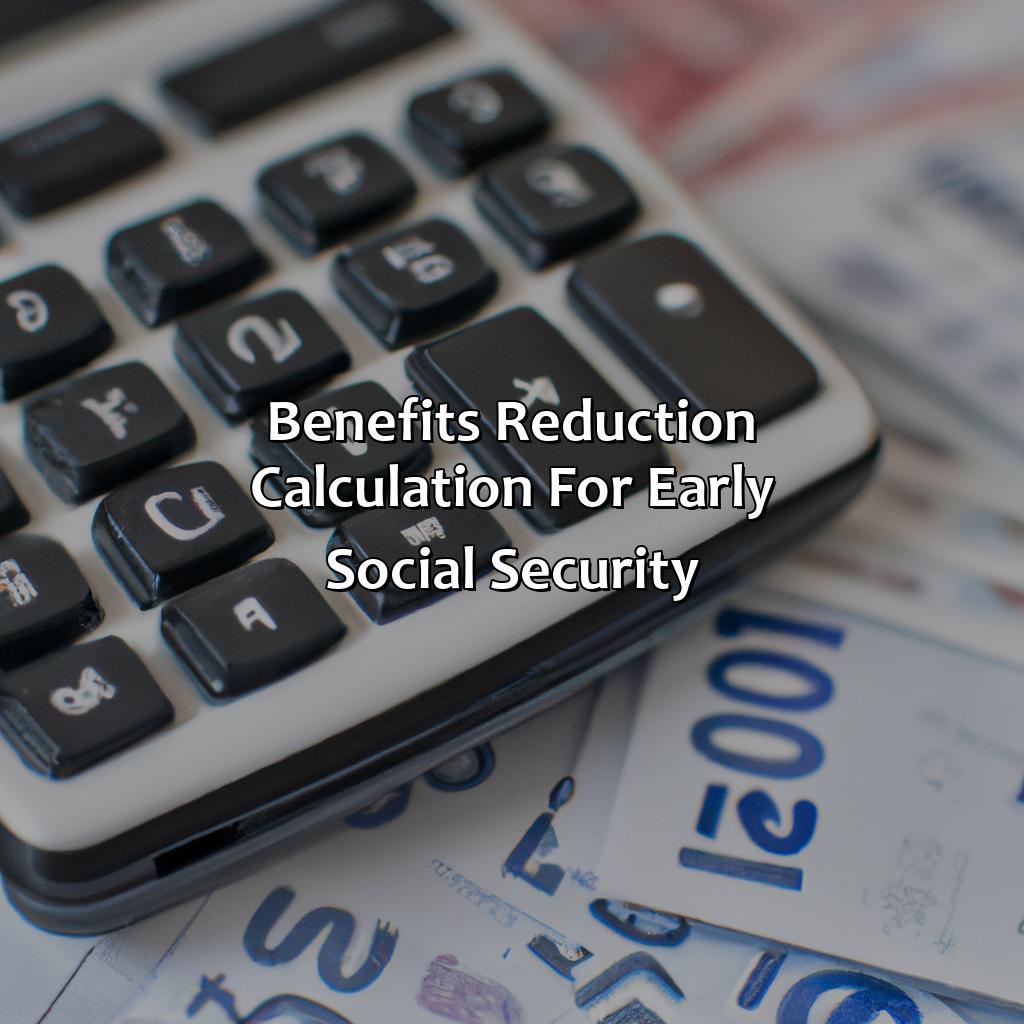

Benefits Reduction Calculation for Early Social Security

Social Security benefits may be claimed early, but this could result in a reduced amount. To understand how much reduction you may experience, consider examining the “Benefits Reduction Calculation for Early Social Security,” which can help determine the optimal strategy for claiming social security early.

Below is a table outlining the “Benefits Reduction Calculation for Early Social Security.” It illustrates how much your monthly benefits may decrease based on when you start receiving benefits compared to your full retirement age.

| Age to Start Benefits | Percentage Reduction |

|---|---|

| 62 | 30% |

| 63 | 25% |

| 64 | 20% |

| 65 | 13.3% |

| 66 | 6.7% |

It is worth noting that if you choose to receive benefits early and still work, there may be an additional reduction in the amount you receive. At times, it is possible to earn more than a certain amount while receiving benefits, but this will be addressed by the “Earnings Test.” To gain a full understanding of the implications of early benefits, consult with a financial advisor or Social Security Administration representative.

Pro Tip: It is essential to weigh the consequences of early benefits when making long-term financial plans. Consider consulting with a financial advisor to determine the best strategy based on your individual situation.

Image credits: retiregenz.com by James Jones

How to Apply for Early Social Security

Applying for early Social Security? We have two options: online and in-person. Each has their own pros and cons. Let’s look at them briefly.

Online application process – advantages and disadvantages:

- Advantages: Convenience to apply from anywhere and anytime. No need to travel anywhere.

- Disadvantages: Limited assistance available. Difficulties arise in situations such as technical issues or translating documents online.

In-person application process – advantages and disadvantages:

- Advantages: Immediate assistance from professionals available. Chance to discuss the best options with Social Security representatives.

- Disadvantages: Congested waiting rooms and long queue times. Inconveniences, particularly long-distance traveling and time constraints, who live far from their nearest Social Security office.

Image credits: retiregenz.com by Harry Arnold

Online Application Process

The process of applying for early social security is straightforward and can be conveniently done online. Here’s how you can initiate the process without any hassle:

- Access the Social Security Administration website and click on the ‘Apply for Benefits’ option.

- Select ‘Retirement‘, followed by ‘Start Now‘ to begin your application

- Provide accurate information, income details, and supporting documents to complete your application

It is essential to ensure that all details provided are precise. Any errors or omissions could result in delays or even removal from your benefits.

When submitting an early Social Security application, it is crucial to keep regular tabs on its status. Since it may take a few weeks to evaluate your documentation, reaching out should be done promptly in case of any holdups or inquiries about necessary materials.

One anonymous individual shared how they applied online for early Social Security after losing their job due to Covid-19-related layoffs last year. With a little bit of effort, the approval process was almost seamless.

Get ready to make awkward small talk with a government worker as you apply for early social security in-person.

In-Person Application Process

With the In-Person Social Security Application Process, you can apply for early social security benefits. Follow these three steps:

- Find your local Social Security Administration office.

- Make sure you have all the necessary documents, such as your birth certificate and employment history.

- Fill out and submit the application form while answering all the questions truthfully.

It’s important to note that during the In-Person Application Process, you may receive valuable guidance and advice from a social security representative. This interaction could help you optimize your benefit calculation.

Consider booking an appointment in advance to avoid long waiting times. Don’t forget to bring original copies of required documents when visiting.

Furthermore, plan ahead for possible health or mobility challenges that may limit your ability to travel or make appointments in person. When applying in-person becomes difficult, consider other avenues like phone applications or online submissions. These steps will help ensure a smooth early social security application process.

Before claiming early social security, consider if living off of ramen noodles and tap water for the rest of your life is really worth it.

Considerations Before Claiming Early Social Security

Want to take early Social Security? Think about lifetime earnings first! That affects your own benefits, spousal benefits, and survivor benefits. Get it?

Image credits: retiregenz.com by James Woodhock

Lifetime Earnings and Their Impact on Benefits

Your Social Security benefits are heavily influenced by your lifetime earnings. Your income over the years is used to calculate your Average Indexed Monthly Earnings (AIME), which determines the benefits you can receive. The higher your AIME, the more social security benefits you are eligible to claim. It’s essential to consider this aspect before claiming early social security benefits.

Claiming benefits earlier than your full retirement age may result in a reduced amount of benefit payments. Moreover, people with high lifetime earnings will receive lower replacement rates for their Social Security Benefits if they claim early. Hence, it’s crucial to calculate how much you’ll lose in benefits by claiming them early and compare that number to any other sources of available income or savings you may have.

It’s important to remember that calculating and predicting these numbers isn’t easy as many factors can influence your exact payout amount. Several online calculators are available that can assist with planning and determining an optimal strategy for claiming social security benefits.

It’s best not to rush into taking Social Security Benefits without evaluating all possible factors influencing your payout and considering both short and long-term outcomes based on different scenarios. Waiting until full retirement age can help maximize monthly income; however, each individual must analyze their situation and make informed decisions about the ideal time for them to begin claiming Social Security Benefits.

Don’t miss out on critical information when making decisions regarding Social Security Benefits. Consult resources, plan ahead, and weigh all options carefully before taking important steps that may alter your financial well-being in retirement.

Marriage may not always provide happily ever after, but it can provide some financial security with spousal and survivor benefits from Social Security.

Spousal Benefits and Survivor Benefits

Spousal Support and Survivorship Perks are Crucial for Secure Retirement Planning

Married couples can take advantage of Spousal Benefits and Survivor Benefits in case one spouse passes away. These benefits can boost the income of both spouses, even if only one has been working. Spousal Benefits allow the nonworking spouse to collect a percentage of their working spouse’s Social Security payment upon retirement and have access to medical benefits. Meanwhile, Survivor Benefits provide additional financial support for the surviving spouse after a partner’s passing.

Some key points to keep in mind:

- Spousal Benefits are available when married couples reach full retirement age.

- The benefits allowed for spouses is up to half of what their working partner would receive at full retirement age.

- Divorced spouses who were married for at least ten years can also claim spousal benefits if they are still unmarried.

- Survivorship perks give surviving spouses more options on how to use their own Social Security payments as well.

- Single persons who never got married nor had children listed in their social security work history typically benefit less from survivorship perks alone, hence why spousal support is valuable.

- In order to maximize both types of benefits, it may be wise for some couples to stagger claiming strategies by having one spouse make a claim early while the other delays which only applies if both partners made eligible contributions.

Additionally, Spousal Allowances can offer individuals protection against unforeseen future circumstances like disability or death. Suppose someone has not earned enough Social Security credits through employment or acquired wages through consistent childbearing responsibilities; In that case, spousal allowances become critical through secured coverage concerns without affecting your earnings’ worth-related calculations.

It was Marlene and Jim Winnestaffer from Washington state who turned out to owe close to $30,000 to the Social Security Administration (SSA) after Mr. Winnestaffer passed away due to breach of contract concerning filing procedures. Nevertheless, under the SSA’s Widow Benefit program, Marlene was eventually able to receive spousal benefits and manage financial losses effectively.

Final Thoughts on Drawing Social Security Early

Drawing Social Security Early – An Informative Guide

When it comes to drawing Social Security early, there are a few things you should consider. First, know that claiming early can result in a reduction in overall benefits. Second, take note of your individual circumstances, as this decision may have long-term effects on your financial plan.

It’s important to weigh the pros and cons of drawing Social Security early. While a reduction in benefits may be a concern, drawing early could provide much-needed financial assistance. Furthermore, individuals with health concerns may want to consider early draw in case of limited lifespan.

Additionally, consider delaying drawing Social Security if possible. This could result in a larger benefit payout in the long run. Overall, make sure to do thorough research and seek professional advice before making any decisions that may affect your financial stability.

In a real-life scenario, John, 62, chose to draw Social Security early due to unexpected health expenses. While he faced a reduction in benefits, he was relieved to have additional income during a difficult time.

Remember, the decision to draw Social Security early is unique to each individual. Weigh the pros and cons carefully, and seek professional advice before making this important financial decision.

Image credits: retiregenz.com by James Woodhock

Five Facts About How To Draw Social Security Early:

You can start receiving Social Security benefits as early as age 62. (Source: Social Security Administration)

You can start receiving Social Security benefits as early as age 62. (Source: Social Security Administration)- If you begin receiving benefits before your full retirement age, your monthly benefit amount will be reduced. (Source: AARP)

- The earliest age at which you can receive full retirement benefits is currently 66 for those born between 1943 and 1954. (Source: Social Security Administration)

- Taking Social Security early may make sense if you have little or no retirement savings of your own. (Source: The Motley Fool)

- Factors like your life expectancy and employment status may also impact the decision to begin receiving Social Security early. (Source: U.S. News & World Report)

FAQs about How To Draw Social Security Early?

Can I draw social security early?

Yes, you can draw social security early at the age of 62, but keep in mind that your monthly amount will be reduced compared to what it would be if you waited until full retirement age.

How much will my benefits be reduced if I draw social security early?

If you start drawing social security at the age of 62, you will receive a reduced benefit of about 30% less than you would have received if you waited until your full retirement age to start drawing your benefits.

What is the full retirement age?

The full retirement age is the age at which you are eligible to receive your full social security benefits. The age varies depending on the year in which you were born. For those born in 1960 or later, the full retirement age is 67 years old.

What are the benefits of drawing social security early?

The main benefit of drawing social security early is that you will receive monthly checks starting at a younger age. This can be helpful if you need the money or if you plan to retire early. However, keep in mind that your monthly benefits will be reduced.

What are the drawbacks of drawing social security early?

The main drawback of drawing social security early is that your monthly benefits will be reduced for the rest of your life. This means that you will receive less money over the course of your retirement than you would have if you had waited until your full retirement age to start drawing your benefits.

What factors should I consider before drawing social security early?

Before deciding whether or not to draw social security early, you should consider your financial situation, your health and life expectancy, and your plans for retirement. You may also want to speak with a financial advisor to help you make an informed decision.