What Is A Nonqualified Pension Plan?

Key Takeaway:

- A nonqualified pension plan is a retirement plan that does not meet the requirements of the Employee Retirement Income Security Act (ERISA), and is typically offered to executives or highly compensated employees.

- The advantages of nonqualified pension plans include flexibility, no contribution limits, and the ability to customize benefits to meet the specific needs of the company and its employees.

- The disadvantages of nonqualified pension plans include tax implications and lack of legal protection for employees, so it is important to carefully consider these factors before implementing such a plan.

- Types of nonqualified pension plans include deferred compensation plans, supplemental executive retirement plans (SERPs), and equity-based nonqualified plans.

- Eligibility requirements for nonqualified pension plans are generally more relaxed than those for qualified plans, and may vary depending on the specific plan.

- Nonqualified pension plans differ from qualified plans in terms of legal requirements, tax implications, and benefits, and it is important to understand these differences when choosing a retirement plan.

Are you worried about your post-retirement financial security? Find out how a Nonqualified Pension Plan can help you plan and prepare for a secure retirement. You can make the most of your retirement years with the right pension plan in place.

Definition of nonqualified pension plans

Nonqualified pension plans are retirement benefit programs for employees that are not subject to the same regulations as qualified pension plans. These plans are usually offered to executives or highly paid employees as a way to enhance their benefits package. Nonqualified pension plans allow employers to offer more flexible benefits while avoiding the costly administrative and legal requirements of a qualified plan.

Unlike qualified plans, nonqualified pension plans do not have to comply with the Internal Revenue Code’s nondiscrimination rules, which require that the plan must not benefit the company’s highly paid employees disproportionately. Also, the employer does not receive a tax deduction until the employee receives the benefit payment. Nonqualified plans are typically funded by the employer’s general assets, while qualified plans receive specific tax breaks and must be funded with dedicated trusts.

A nonqualified plan can be structured in a variety of ways and may include deferred compensation, stock options, or other types of executive perks. These plans can provide more generous benefits to key employees without having to offer them to all employees, as qualified plans require. However, they may be subject to certain risks, such as the employer’s insolvency or inability to pay the benefits.

According to the Wall Street Journal, in 2018, 75% of Fortune 500 companies offered nonqualified deferred compensation plans to their executives.

Image credits: retiregenz.com by Adam Duncun

Advantages of nonqualified pension plans

Discover the benefits of nonqualified pension plans! They offer flexibility, no restrictions on contributions, and the ability to customize. This makes it possible to tailor the retirement plan to satisfy both employer and employee. So, if you want to learn more, read on!

Image credits: retiregenz.com by David Arnold

Flexibility

Nonqualified pension plans offer adaptability in terms of plan design and benefit structure. They are flexible enough to cater to the specific needs of highly compensated employees. These plans are not subject to ERISA regulations, providing greater flexibility in investment options, benefits distribution, and vesting schedule.

Moreover, nonqualified pension plans can be customized without requiring the approval of all participants or meeting certain funding requirements. This freedom allows companies to create more personalized retirement solutions for executives who have unique circumstances that cannot be addressed by standard qualified retirement plans.

Companies can also adjust benefits or contributions based on the employer’s financial capacity or changes in the employee’s compensation. This feature is especially useful for startups or small businesses that may face financial constraints initially, but have growth potential in the future.

Companies can also use pension schemes as a tool to recruit and retain top talent. Offering competitive retirement benefits would attract skilled professionals, resulting in a better workforce and improved business performance.

According to MSCI ESG Research LLC., companies providing generous nonqualified pension benefits for executives generally see positive effects on their overall corporate reputation. Money talks, but in nonqualified pension plans, there’s no limit to how loud it can scream.

No contribution limits

One of the significant benefits of opting for nonqualified pension plans is the absence of restrictions on contributions. This allows employers and employees to contribute an unlimited amount towards retirement savings, unlike qualified plans that have limits. Nonqualified plans provide flexibility in terms of contribution amounts, as both parties can decide on the amount to be contributed based on their financial capabilities and needs.

In addition to this, pension funds also offer greater customization options than qualified plans. Employers can design a plan that suits their specific needs and requirements while tailoring it to attract and retain top talent. Unlike qualified plans, nonqualified ones do not come with strict regulations regarding age or income criteria. Thus, they are ideal for companies seeking customized strategies to meet their retirement goals.

Unlike Qualified Pension Plans, which must abide by federal laws and regulations under ERISA (Employee Retirement Income Security Act), Nonqualified Pension Plans offer greater flexibility in deciding when payout will occur.

If you are wondering how does a pension work in the UK, understanding the difference between qualified and nonqualified pension plans is a great place to start.

To further demonstrate the benefits of nonqualified pension plans- one Fortune 500 company established a NQDC Plan in 2007 for select executives who deferred compensation into the program before experiencing life changes such as disability or termination. This safeguard increased retention rates among high-ranking employees and allowed them to accumulate additional funds while reducing taxes during high earning years.

When it comes to nonqualified pension plans, you can personalize your benefits package like a burger at a fast food joint – hold the lettuce, extra cheese, and a side of retirement savings.

Ability to customize benefits

The ability to tailor the benefits of nonqualified pension plans is one of its most significant advantages. Employers can customize these plans to suit specific employee needs and better attract and retain top-talent.

- Employers can design customized vesting schedules, which encourage employee loyalty.

- Employers can choose to offer higher contribution limits or match contributions, depending on the level of employee seniority or income.

- The plan’s flexibility allows employers to adapt to specific circumstances like mergers or acquisitions, restructuring, or changes in company strategy.

- Nonqualified pension plans are not subject to ERISA rules and regulations, so employers have more freedom regarding benefit design. For example, they may decide to offer benefits that exceed qualified plan limits.

- Pension plans may include non-financial benefits like employer-paid medical premiums, retirement planning assistance and education programs that fulfill their employees’ unique needs.

While traditional 401(k) plans tend to be cookie-cutter with limited customization options, nonqualified pension plans allow companies more flexibility and creativity in developing unique plans. These customized nonqualified pension plans help them align with business goals by driving retention rates, recruitment efforts, and enhancing overall employee satisfaction.

It wasn’t until 1954 that Congress introduced the first piece of legislation allowing tax deferral on nonqualified pensions. Since then these pension arrangements have become widely used by large corporations as a reward for retaining top executives while reducing the firms’ tax liability.

Nonqualified pension plans may offer advantages, but let’s not forget the saying ‘what goes up, must come down’ – and that includes your retirement savings.

Disadvantages of nonqualified pension plans

Do you know the downfalls of nonqualified pension plans? It’s time to dive deep and learn! Tax implications and lack of legal protection are two disadvantages that come with this retirement choice. These could impact your financial stability and security, so it’s important to be aware.

Image credits: retiregenz.com by Joel Arnold

Tax implications

When it comes to nonqualified pension plans, the tax implications can be significant. Withdrawals from such plans are subject to income tax, and sometimes additional taxes, depending on various factors. Additionally, contributions to a nonqualified plan are not tax-deductible for the employer.

As nonqualified pension plans do not have to adhere to the same Internal Revenue Service (IRS) regulations as qualified plans, this reduces their attractiveness for both employers and employees. For example, the retirement benefits of a nonqualified plan can be reduced or even eliminated at the discretion of the employer. The lack of portability is another issue with these plans if an employee leaves their job before retirement, they often cannot take their benefits with them.

One unique detail is that some high-income earners may use a nonqualified plan in addition to a qualified plan as a way to save more for retirement beyond what the IRS limits allow in a qualified plan alone. Are you curious about what is CAAT pension plan? Learn more here.

Overall, while there may be specific circumstances where a nonqualified pension plan makes sense, such as for highly compensated executives or business owners looking for more flexibility in retirement benefit design, most employers and employees will likely find greater tax advantages and stability with qualified plans. Don’t miss out on potentially higher returns and better savings opportunities by solely relying on a nonqualified pension plan.

You’ll have better legal protection as a cartoon character than you will with a nonqualified pension plan.

Lack of legal protection

Nonqualified pension plans are not protected under the Employee Retirement Income Security Act (ERISA). This means that they lack legal protection, making them riskier for employees to invest in compared to qualified plans. In nonqualified plans, employers have more control over the funds, and there is no federal insurance or guarantee of payment. Therefore, if an employer faces financial difficulties or bankruptcy, the employee’s benefits may be at risk.

It is important for employees to carefully consider the terms of a nonqualified plan before investing in it. They should assess the financial stability of their employer and review the details of the plan carefully. Additionally, employees may want to consult with legal professionals before committing to a 501(C)(18)(D) pension plan.

Pro Tip: While nonqualified pension plans offer flexibility and other unique benefits, they come with increased risks. Consider seeking guidance from financial advisors and legal professionals before signing up for a nonqualified plan.

No qualifications needed for these nonqualified pension plans, just a willingness to retire poor.

Types of nonqualified pension plans

Discover more on nonqualified pension plan types! There’re three sub-sections to explore:

- Deferred compensation plans

- Supplemental executive retirement plans (SERPs)

- Equity-based nonqualified plans

Check out the section ‘Types of nonqualified pension plans‘ for more info!

Image credits: retiregenz.com by Adam Duncun

Deferred compensation plans

Non-qualified pension plans, commonly known as deferred compensation plans, are an alternative to traditional qualified retirement plans offered by employers. These types of plans allow highly-compensated employees to defer a portion of their income for retirement without being subject to the same restrictions as traditional qualified plans.

Unlike qualified plans, which must adhere to strict IRS guidelines and limits, non-qualified plans can be tailored specifically to meet the needs and goals of individual employees and employers. Contributions made by the employee are generally not tax-deductible until the funds are withdrawn, usually at retirement. Additionally, these plans are typically funded solely by the employer and may offer benefits like supplemental executive retirement plans (SERPs), excess benefit plans (EBPs), or phantom stock appreciation rights (SARs).

It’s worth noting that a public pension carries certain benefits that non-qualified pension plans do not. For example, public pensions are typically funded by the government and have guaranteed benefits. On the other hand, non-qualified pension plans carry risks that traditional qualified retirement accounts do not. Since contributions are not tax deductible until withdrawal, they can be subject to changes in tax law or rates. Additionally, since the benefits promised under these types of arrangements are unsecured obligations of the employer, there may be concerns about the long-term viability of any particular plan.

Overall, while non-qualified pension plans may offer greater flexibility and customization than traditional qualified accounts, it is essential to consider all factors before committing to a specific plan. Missing out on potential benefits due to unforeseen risks could have a dramatic impact on one’s long-term financial future.

Why wait until retirement to live like an executive when SERPs can let you do it now?

Supplemental executive retirement plans (SERPs)

Supplemental plans for retiring executives with high salaries and benefits in excess of qualified pension plan limits are known as alternative executive retirement plans (AERPs). AERPs, often referred to as top hat plans, are unfunded arrangements that provide additional retirement income for executives.

These non-qualified retirement plans have a significant impact on executive compensation. It offers the benefits of deferred compensation to senior executives outside of standard ERISA regulations. With an AERP, executives can invest their deferred money in a company stock that grows until they retire from the company.

The attractiveness of these plans lies in their flexibility, which allows personalized benefit structures. The employer is free to choose who receives benefits and how much these DC pension plan benefits will be. However, it ought to be transparent about plan eligibility conditions and its financial risks.

Companies must remember these non-qualified pension schemes aren’t guaranteed by the Pension Benefit Guaranty Corporation (PBGC) that guarantees qualified pensions’ payment upon employer bankruptcy or defaulting employees’ obligations under PBGC policy premiums.

Why wait for retirement to lose all your money in the stock market? Try an equity-based nonqualified plan today!

Equity-based nonqualified plans

Nonqualified pension plans that provide equity-based compensation to executives or highly compensated employees are known as Equity-based nonqualified plans. These plans offer a way for companies to reward key personnel for their performance without conforming to the rules of qualified plans. Called deferred compensation, this form of nonqualified plan pays out retirement income at a later date, thus evading taxation and benefiting those in higher tax brackets.

Such non-qualified plans may include stock appreciation rights, phantom stock, or restricted stock units. The participants benefits are usually linked with the company s stock and increase as the firm’s share price goes up. However, unlike qualified retirement plans, participants must bear the risk of losing value if the company’s shares decline.

As these types of plans only cater to high-earning executives, it is essential for companies to structure them in ways that do not discriminate against employees otherwise they would fail the non-discrimination testing rules. Companies must maintain transparency surrounding such rewards and emphasize reliable financial planning to ensure proper communication is established between administrative teams and beneficiaries.

Missing out on certain company benefit opportunities could lead to demand mishap or even legal problems down the line. Incentivizing vital members of your company through unique benefit schemes like Protected Pension Rights can motivate teams and take your business to new heights.

Sorry, kids, you can’t join the nonqualified pension plan club unless you’ve already maxed out your 401(k) and have a deeply ingrained fear of paying taxes.

Eligibility requirements for nonqualified pension plans

Nonqualified pension plans have different eligibility criteria compared to qualified plans. These plans mostly target top executives and high-income earners who might not satisfy the requirements of qualified plans. These plans are exempted from ERISA guidelines, thus providing greater flexibility in plan design and funding options.

The participant must be an executive with compensation exceeding the IRS limits to be eligible for a nonqualified plan. Employers can distinguish between eligible and ineligible employees based on their discretion. These plans do not have contribution limits and offer flexibility in the benefit payment options. To know more about pension plans, check out money purchase pension plans.

Nonqualified plans are not backed by FDIC protection, and participants have unsecured claims against the employer s assets. These plans don’t follow the anti-discrimination rules, meaning that high-level employees can receive a larger benefit than lower-level employees.

Employers can offer benefits to select employees, who may not qualify for other retirement plans. However, nonqualified plans have higher associated risks. Employers may consider alternative retirement savings accounts or Roth 401(k) plans to diversify the retirement portfolio of executives. This approach also helps in circumventing the negative public perception of offering amenable benefits to higher executives.

Image credits: retiregenz.com by Harry Jones

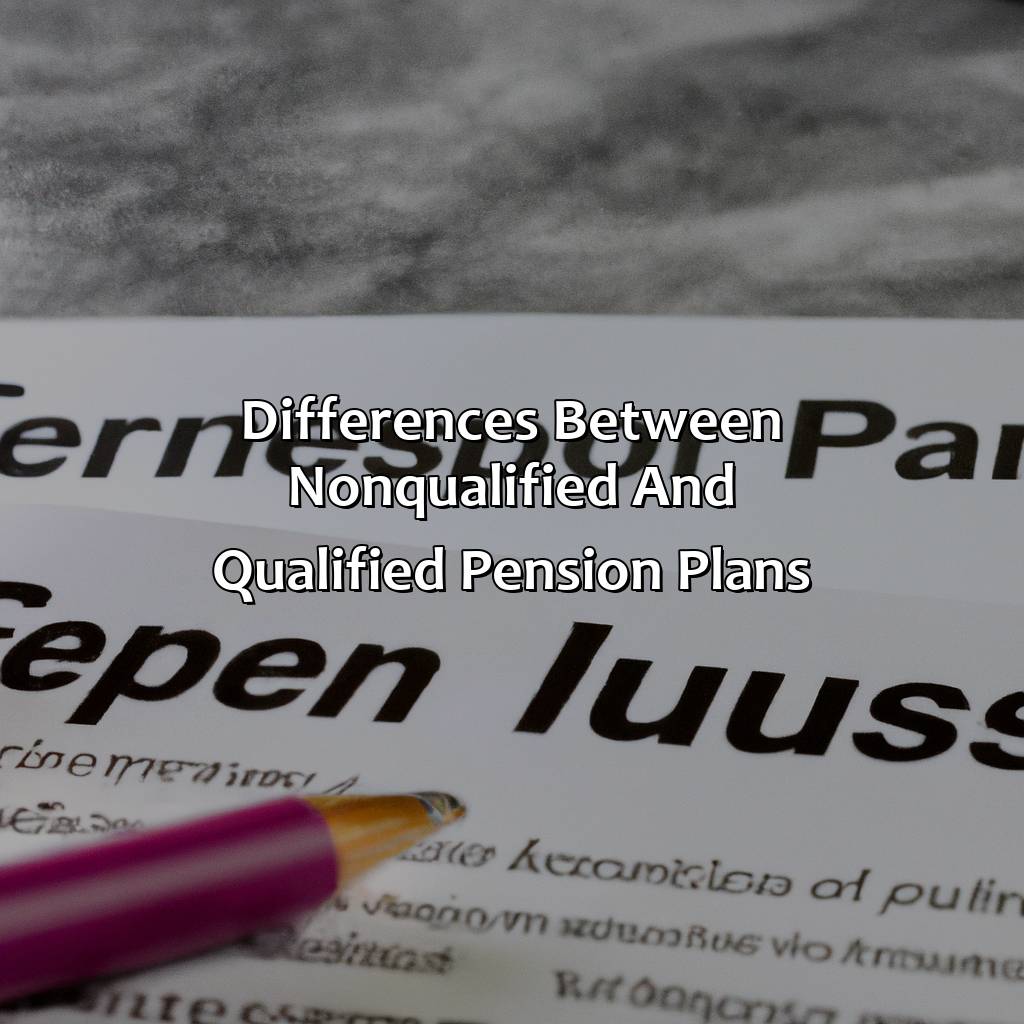

Differences between nonqualified and qualified pension plans

When it comes to retirement plans, there are two main categories to consider – qualified and nonqualified pension plans. The primary difference between these two plans is that qualified plans are governed by ERISA (Employee Retirement Income Security Act) and offer tax benefits to both employers and employees, while nonqualified plans do not have the same legal requirements or tax advantages. To better understand the differences, take a look at the table below:

| Qualified Plans | Nonqualified Plans |

|---|---|

| Covered by ERISA | Not covered by ERISA |

| Tax-deductible contributions | No tax advantages for contributions |

| Participant contribution limits | No contribution limits |

| Investment options limited by plan | Greater flexibility and choice in investments |

| Required to offer benefits to all employees | Can be designed to benefit only select employees |

| Protected from bankruptcy | Not protected from bankruptcy |

It’s important to note that nonqualified plans can still be a valuable tool for retaining top employees and providing additional retirement benefits beyond what qualified plans allow. However, they require careful planning and consideration of the potential risks, such as the lack of legal protection in the event of bankruptcy. Ultimately, the decision of whether to offer a nonqualified plan should be based on the specific needs and goals of an organization. Consulting with a financial professional can help ensure that any retirement plan is designed to meet the unique needs of an employer and its employees.

Image credits: retiregenz.com by Harry Woodhock

Some Facts About Nonqualified Pension Plans:

- ✅ Nonqualified pension plans are retirement plans that do not meet the requirements of the Employee Retirement Income Security Act (ERISA). (Source: The Balance)

- ✅ Nonqualified pension plans are offered by employers to top executives and highly compensated employees. (Source: Investopedia)

- ✅ These plans allow for greater flexibility than qualified plans, but also come with greater risk for participants. (Source: The Motley Fool)

- ✅ Unlike qualified plans, nonqualified pension plans do not provide the same tax benefits for employers and employees. (Source: Forbes)

- ✅ Employers can design nonqualified pension plans to fit their specific needs and goals, but must comply with certain rules and regulations. (Source: The Hartford)

FAQs about What Is A Nonqualified Pension Plan?

What is a nonqualified pension plan?

A nonqualified pension plan is a retirement savings plan that is not subject to the same rules and regulations as a qualified plan, such as a 401(k) or a traditional pension plan. Instead, nonqualified plans are set up by employers to provide retirement benefits to key employees or executives.

What are the advantages of a nonqualified pension plan?

Nonqualified pension plans offer several advantages, including greater flexibility in benefit design, no contribution limits, and the ability to provide benefits to highly compensated executives who may not be able to participate in a qualified plan due to IRS contribution limits.

What are the disadvantages of a nonqualified pension plan?

One major disadvantage of a nonqualified pension plan is that they are not protected by ERISA, so there is no guarantee that the employer will offer the promised benefits. Additionally, nonqualified plans are typically unfunded, meaning that the employer is not required to set aside money to pay for future benefits.

How are nonqualified pension plans taxed?

Nonqualified pension plans are taxed differently from qualified plans. Employer contributions to a nonqualified plan are not tax-deductible until the employee receives the benefit. Additionally, employees are taxed on the contributions and earnings in the year they receive them, rather than when they are contributed.

Who is eligible to participate in a nonqualified pension plan?

Nonqualified pension plans are typically designed for highly compensated executives who may not be able to participate in a qualified plan due to IRS contribution limits. Employers may also offer nonqualified plans to key employees as a retention tool.

How do nonqualified pension plans differ from 401(k) plans?

Nonqualified pension plans differ from 401(k) plans in several ways. Nonqualified plans are typically unfunded, while 401(k) plans are funded through employee contributions. Nonqualified plans also offer greater flexibility in benefit design and are not subject to the same contribution limits and other rules as 401(k) plans. However, nonqualified plans are not protected by ERISA, so there is more risk involved in terms of receiving promised benefits.